Written FOR dummies BY dummies!

Have you tried taking financial advice from successful millionaires and billionaires? I have. Have any of their strategies worked? Not really for me. I mean I’m not a millionaire or billionaire afterall. Also, just like exercising regularly, I don’t stick with it. I thought ‘Well, she/he’s a millionaire, they must be able to tell me something so that I can be a millionaire too.’ I don’t mean to bad mouth anyone. Honestly, it’s me. I’m a bit inconsistent and self deprecating. I’m not competitive and so when the financial going gets tough, I tend to hide in a cave and tone it down a notch rather than “get going” like a tough guy.

Some of these millionaire programs first ask to fork out money. It’s either for a membership to their exclusive club in which they will divulge all their strategies. Or money for their program. Something that I had to pay for in order to get some advice for getting on track. But I just needed to get on track. I wasn’t in a head space to become a millionaire or billionaire. I needed to get back on track.

Soooo, have you ever tried taking financial advice from a dummy? I did, a couple of years ago. And I learned more from those people for free. I’m not great with money but I have learned from people who were worse than I was. I’ve learned from people who are better than me too. I learned from both types. And they weren’t millionaires. Both made me realize things about myself. Habits I had, GOOD ONES, and bad ones. Boundaries I had and habits and boundaries that I needed to create.

Hello, dummy! It takes one to know one. OK, you don’t really know me, but trust me, I’m a dummy.

I want to share with you some simple and FREE habits and strategies I have been practicing over the past 2 years which have helped me lower my anxiety on payday AND turn myself around to controlling my money instead of it controlling me.

In this article I want to share just one. The first and single most simple habit I have been practicing that helped me start controlling my money within 3 months. KNOWLEDGE is power. I honestly had very little knowledge about what my money was doing and where it was being spent. I just knew that I didn’t have enough and before the month was over, my money was gone and I was eating peanut butter from the jar and bundling up at home instead of running the heat.

You’ve heard of the straw that broke the camel’s back? Well this camel’s back was broken many times. Cue the music “I get knocked down, but I get up again, they’re never gonna keep me down.”

One of my mantras is to be like the palm tree. Bending with the storm then bouncing back unbroken. In 2018, however, another straw broke the camel’s back again and this time I filed for divorce. This left me in over my head in debt because when he moved out, I then had to pay for everything. I wasn’t sure I made enough to do that but I thought maybe I did? And this is why I need to control my money. He was out of the picture and couldn’t control nor influence any of my finances so, that was good. I had only myself to rely on. There was no one and nothing else going on behind my back. That made things more manageable.

I’m a teacher. I have a good, secure job and good pay. My pay was not impacted at all during the COVID lockdown so I have that going for me. In fact, conducting distance learning from home freed up over $300 month for me because I was working at a school one hour from my home. The gas alone was a savings for me. I know the gas was this much because of the habit I’m about to share with you now.

STEP #1

TRACKING YOUR MONEY

I have been calling it this up until a couple of months ago when I discovered that the Japanese call it keikebo. Not only is that a way cooler name but I was pleasantly surprised to make a connection with the ancients. Once again, the reason I began this blog is to share ways in which we are all interconnected in every way possible. So I’ve been calling it keikebo ever since.

When I ventured out on my own in 2018 my mortgage was about ¾ of my salary. That left me only ¼ of my salary to pay my monthly bills and then- well then-I just went on with a wing and a prayer that the money would stretch to the end of the month. Because I was a dummy.

There were other strategies and practices which I also started. I am working on another blog post to share those with you. Here, today, I want to share the very FIRST step I took toward controlling my money and gaining KNOWLEDGE. And we all know that KNOWLEDGE is POWER.

Tracking all my spending immediately lead me to becoming more mindful of the number of stops I was making to spend my money. I actually LISTENED to the cashiers when they told me the total. I had a conscious thought…”hmmm, that seems high for just these things.” or “oh, that’s not too much, I thought it would be more.” Does this happen to you? We are not alone. I have a friend who had bought a few groceries which included 2 loaves of challah bread and the cashier errantly rang her up for 63 loaves and she blindly just paid it and walked out without noticing until she got home! I know there have been PLENTY of times I’ve gotten to my car completely oblivious to what my grocery bill was just moments before. I just slide my card like a zombie without even listening or thinking. It’s that numbing mindset that “Well, I need food and groceries so I just pay whatever they say to pay. It’s not like this is something I can control.” But that is WRONG. KNOWLEDGE is power. KNOWING what you are spending is the first baby step to take control and change (if change is needed.)

This practice made me a little anxious. But not so much that I didn’t want to continue. It caused me just enough anxiety that I avoided stopping for many days. I tried to see how long I could go without spending any money. Not stopping on a whim made me store up and stop 2-3 places on one day instead of stopping to spend money every day. Storing up made me think more about what I needed to buy and thus shop with more of a shopping list and more of a purpose. Shopping with a list and purpose cut down on my spending.

Here’s all you need.

1- A pocket calendar/planner from the Dollar Store.

2- A notebook-also from the Dollar Store OR a digital spread sheet (here’s a free download)

|  |

The Pocket Calendar:

Go to the Dollar Store and buy a small pocket planner. Don’t spend a lot of money on anything cute or fancy. Do pick an available color that tickles your fancy. Something that is joyful and pops out, so you always know where it is. (Last year I used red because it’s my favorite color. This year I chose this color that reminds me of the sea.) Put it where it will always be handy.

|  |

I keep mine in the center console of my car. (During COVID lockdown this didn’t work well because I did way more buying on line.) So, please find a place that makes entering your receipts seamless. If you’re a dummy like me, you will skip entering expenditures if this planner (rebranded Keikebo) is not at your finger tips at the right time. Full disclosure, I still miss entering my online purchases. I am finding that I only catch them at the end of the month when I complete step #2.

You are going to enter EVERY RECEIPT you get. Just jot it down on the date and categorize it. Is it for groceries, a gift, gas, clothing, etc? Then throw away the receipt (unless you think you’re going to need it later.) When the cashier asks you “Do you want the receipt printed or emailed? In the bag or in your hand?” The answers are “PRINTED PLEASE” and “in my hand. “

Now, I will give you the choice. Choice #1- With receipt still in hand, you either enter it in your keikebo before you put the key in the ignition OR Choice #2- put it in the planner and drive off. When you get home, you do not get out of the car until you enter all your receipts (even if it’s just one) into your keikebo. Then throw away the receipt(s).

That’s it.

Baby step #1.

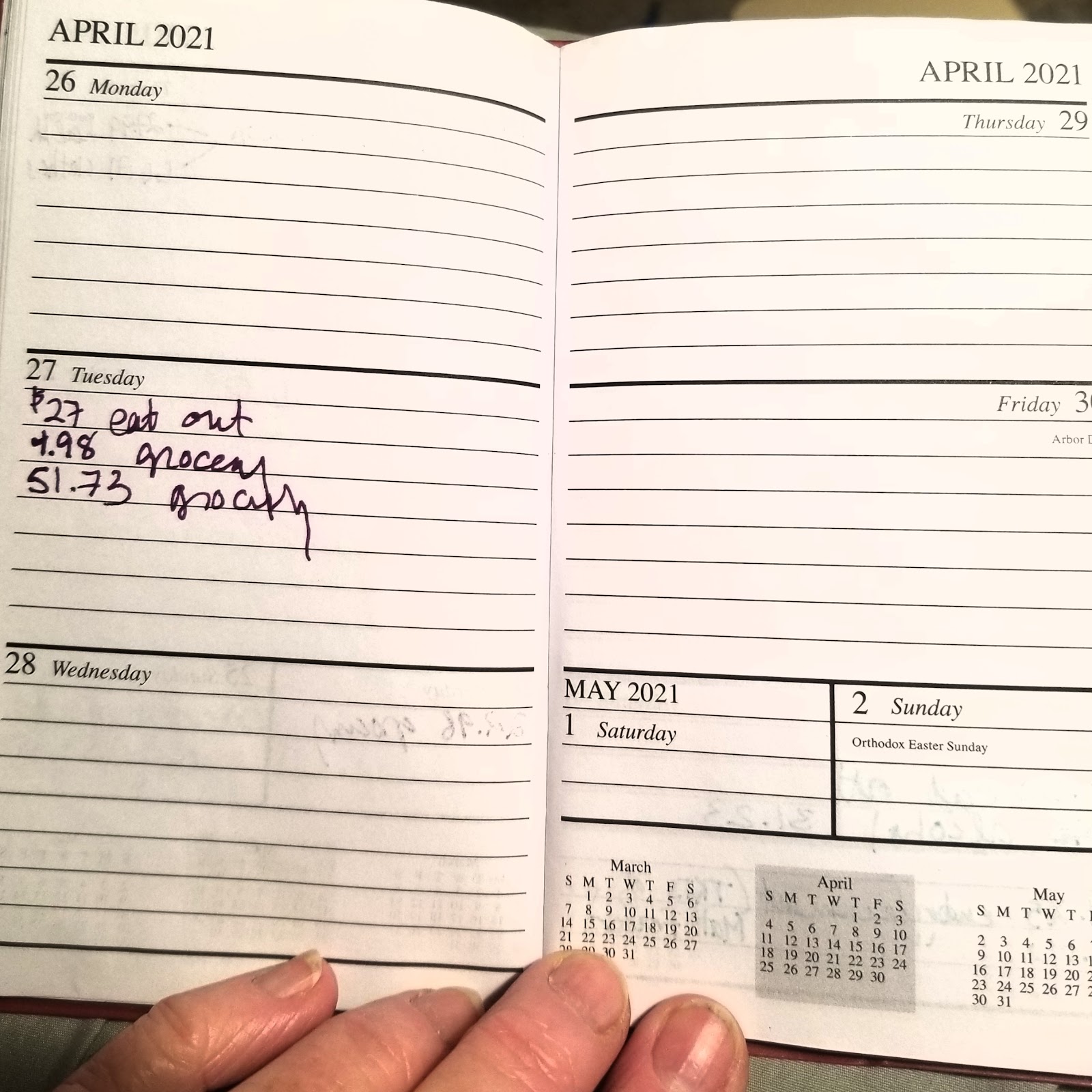

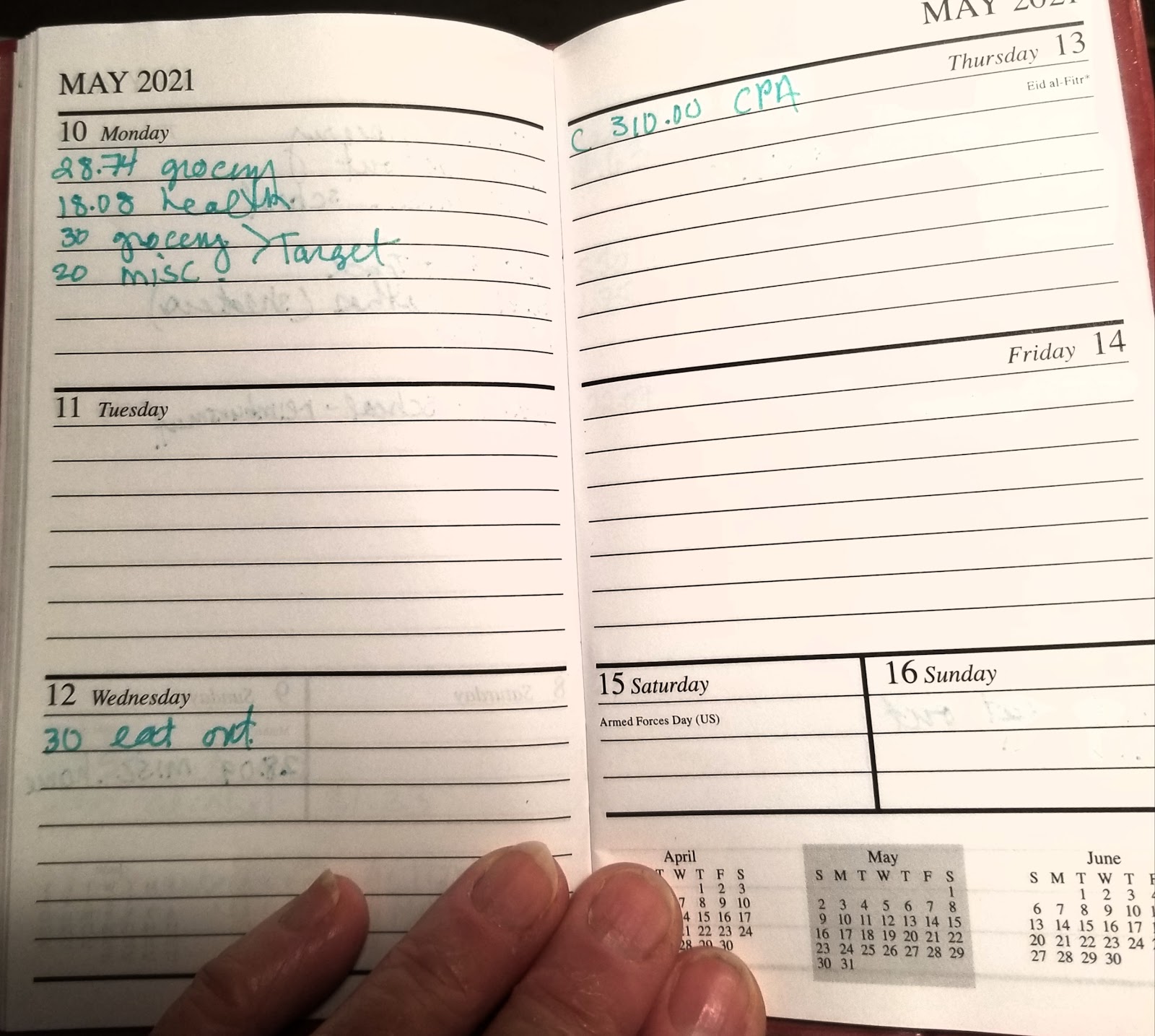

Here are some random pages from my very simple keikebo. It shows how I have consolidated my spending days.

|  |

|  |

Before you go on to step #2, now is a good time to take a break from reading and either contemplate what I’ve written and/or watch this interesting youtube video about the concept of Keikebo. I really liked it. It reinforced what I had been doing for about two years. My savings came naturally without any goals, but I will write about that in a later post.

STEP #2

The Ledger/Spread sheet

I use Google sheets but you can use a notebook or Microsoft spreadsheets.

Again, nothing fancy. Any plain notebook will do. I have provided a free digital download for you. (Please free to contact me if you need steps to duplicating pages at the bottom and renaming them. It’s a simple right click on your mouse pad and readily available information on Google help, but, I’m always glad to hear from you.)

My sister was my accountability partner on this. In fact it was her idea. Do you have someone you can trust to hold you to making this a constant habit?

Full disclosure here. My sister told me about this and how it helped her. She sent me a sample blank spreadsheet. She encouraged me to do it for me, that she had no interest in knowing my specific finances and had no intentions of judging me, she didn’t want the numbers. She just wanted me to do it so that I myself had the numbers. I couldn’t (and wouldn’t) have done it without her. She asked when I would be starting it and when she could expect a copy or notification that I did it. I gave her something like 3 weeks because she was very persistent. Well, 4 weeks later, I had a voicemail from her saying-this is pretty much a direct quote- “Marisa, this is your sister. I’m calling because you said you’d have this ledger going after 3 weeks and it has been 4 weeks. I haven’t received anything from you showing that you started it. You are the one who said you’d be starting it. I’m just calling to check to see if you did what you said you were going to do. It’s for you after all, not me. You are the one who said you needed to get control. I’m just calling to find out if you are doing that.” Do you have someone in your life who can be direct like that? Why not give them this exact script so they can remind and encourage you?

I remember one of the months I got lazy with it and started stressing about backtracking to fill in the prior month when I was well into the current month. At the beginning, I did it for 1-2 months, then skipped and got sloppy about entering receipts. My anxiety rose as I thought about the daunting task of going back and filling in the month I skipped. And then what would I tell my sister and accountability partner?! When I told her I was behind she graciously said ‘fuggetaboutit.’ Forget about backtracking. Just give yourself grace, you’re new at this, just forget last month and pick it back up THIS month. Forget it. Don’t bother.

If you try this simple habit and in the beginning neglect it, advice from this dummy is to just get back on track with the current month. Keep going forward and don’t look back. Just keep moving forward.

After about 6-7 months this was a part of my life, #1) a daily routine of entering every receipt into my keikebo and #2) a monthly routine of transferring everything from my keikebo into the ledger. (I get paid once a month and this financial stuff-right up there with exercising regularly-is not my favorite adulting responsibility, so I have always balanced check books and paid bills only once a month.)

After a few months of entering the category totals I cringed at the amount I was spending on groceries. I tried to cut back a little more the following month but it still came out about the same. With about 5 consistent months in my ledger, I asked around. I asked a bunch of friends how much they spend on groceries. Guess what. Not ONE single ONE of them had any idea. Pat on the back for me! I felt like I was a step ahead of a bunch of people in this game. That was exciting!

Since my friends were no help, I looked at some of my habits. One thing I noticed was that I had a lot of containers with left overs and was throwing out a lot of food that had gone bad in the fridge. I was cooking for just my son and me. Turns out not only was I was cooking too much food for just us but in working hard to maintain normalcy for my son by cooking new meals every day I hadn’t factored in this new routine of custody. Often I would make a new meal when there was a refrigerator full of leftovers and then he’d be gone for a few days. I changed that habit. I made sure I cooked bigger meals on the day he came home and I became better and disguising leftovers or using leftovers in a completely different way. I became a better meal planner all ‘round.

It has been two and a half years now and this one baby step quickly lead to a few others simple changes which I will write about next month. Since I keep every month in the bottom tabs of the google spreadsheet, it’s very easy to click on past months to see what I spent in different categories and compare. (For example, I can click on December 2020 and see just how much I spent on Christmas gifts last year. That gives me a ballpark for what I can expect this year.) Though I have made other changes (and one very significant one) the money I have left over AFTER paying my mortgage and bills has quadrupled. You heard that right, I have a growing savings account! I guess I can officially say that I’m not living paycheck to paycheck because I have money left over at the end of the month!

TIME & GRACE

Give yourself some love and time. Honestly, I was a hot mess at payday. I knew I needed a payday but my anxiety was also high so when my paycheck arrived instead of a sense of relief, I suddenly then got nervous. Why? Because I knew my money was controlling me instead of ME controlling my money. I knew I earned enough to pay all my bills but then I stressed about all the groceries and absolutely anything else that might come up during the month. Everything else was out of my control. Groceries, gas and incidentals. I just stayed on this step for over a year. I’m a dummy-I told you that in the title.

Would you do me a favor and share your ideas about this one strategy here in the comments? Could you also follow me on facebook and share this post with your own social media on instagram, twitter, facebook or elsewhere? Whether or not this is a helpful strategy for you, you never know who in your circle might benefit from this baby step.

UPDATE:

THIS selfie shows WHY you want to enter receipts daily. This pic ALSO shows why you want receipts in your hand and NOT in the bag! Here I said that I really don’t stop often nor spend money every day. This represents only about two weeks of receipts. Just look how they pile up! I have been a little lax this month entering receipts in my keikebo and instead have been shoving them into my wallet. As usual, I don’t even have any actual money in my wallet, just receipts.